Most people sign an auto loan at the dealership under time pressure, surrounded by paperwork, and often accept a rate that’s higher than what they’d qualify for if they shopped around. Refinancing an auto loan gives you a second chance to fix that — and in many cases, it can trim hundreds or even thousands of dollars off what you ultimately pay.

The process is simpler than most borrowers expect, but it requires honest timing, a clear understanding of your credit profile, and a realistic look at the numbers. This guide walks through exactly how to do it right.

What Auto Loan Refinancing Actually Means

Refinancing an auto loan means replacing your current loan with a new one — usually from a different lender — that carries better terms. The new lender pays off your existing balance, and you begin making payments under the new agreement. The goal is almost always one of three things: a lower interest rate, a reduced monthly payment, or both.

It’s worth separating the two outcomes because they don’t always come together. A lower rate with the same remaining term reduces your monthly payment and your total interest. Extending the loan term can reduce your monthly payment even without a lower rate — but it increases the total amount you pay over time. Shortening the term does the opposite: higher monthly payments, but significantly less interest across the life of the loan.

Understanding which outcome you’re actually chasing prevents a common mistake: people refinance to feel relief from a high monthly payment, unknowingly extending their loan by two years and paying an extra $1,200 in interest in the process. Define your goal before you talk to any lender.

It also helps to understand what refinancing is not. It’s not the same as trading in your vehicle or taking out a personal loan to cover your balance. You’re working within the existing structure of an auto loan — the car remains collateral — but negotiating better terms based on how your financial profile has changed since the original agreement was signed.

When Refinancing Makes Financial Sense

Timing matters more than most guides admit. Refinancing works best when at least one of the following conditions is true:

- Your credit score has improved significantly since you took out the original loan. Even a 40-point increase can unlock a meaningfully lower rate tier with most lenders.

- Market interest rates have dropped. If your original loan was written during a high-rate environment, today’s rates may be considerably lower — though in 2024–2025, rates remain elevated, so this requires careful comparison.

- You originally financed through a dealership and suspect the rate was marked up. Dealers routinely add 1–2 percentage points to the rate they receive from lenders, keeping the difference as profit.

- Your debt-to-income ratio has improved. A new job, a paid-off credit card, or reduced recurring debt can shift you into a more favorable underwriting bucket.

There are also situations where refinancing doesn’t make sense. If your loan is nearly paid off — say, within 12 months — the administrative friction and any origination fees will likely outweigh the interest savings. Similarly, some lenders charge prepayment penalties, so check your original loan agreement carefully before proceeding.

One more scenario that’s easy to overlook: if your vehicle has depreciated significantly and you now owe more than it’s worth, many lenders will decline to refinance. Loan-to-value ratio is a key underwriting factor — lenders want assurance that the collateral justifies the loan amount. If you’re in that position, aggressively paying down the principal for a few months before applying may open more doors.

How Much Can You Actually Save?

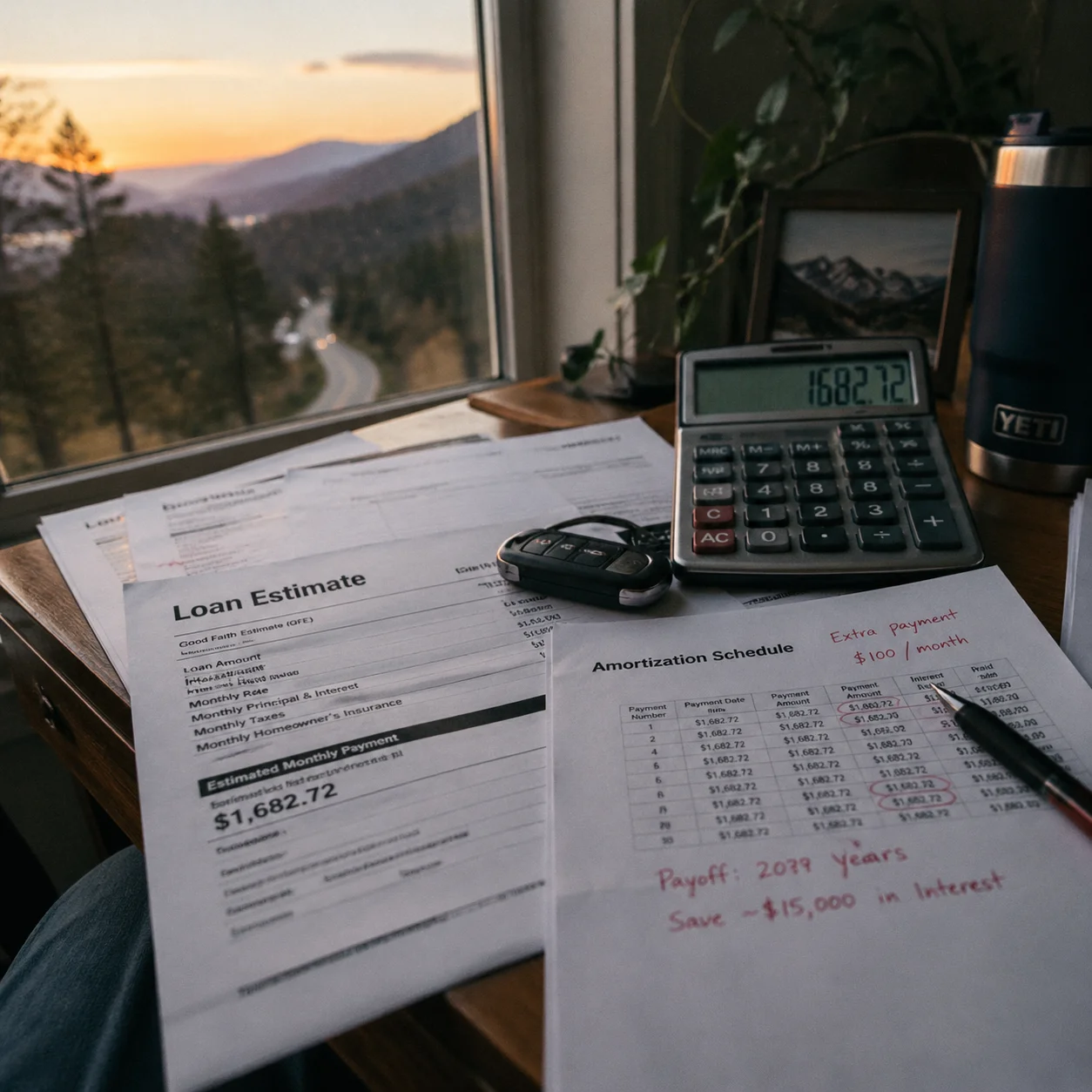

Let’s ground this in a real scenario. Suppose you financed $25,000 over 60 months at 9.5% APR — a rate common for borrowers with fair credit at a dealership in 2023. Your monthly payment would be approximately $524, and you’d pay roughly $6,440 in interest over the life of the loan.

Now imagine you refinance 12 months in with a remaining balance of around $21,200. A credit union offers you 6.2% APR on the remaining 48 months. Your new monthly payment drops to about $499, and you’d pay roughly $2,700 in interest from that point forward — compared to about $4,800 if you’d stayed on the original loan. That’s over $2,000 in savings, achieved with one application.

According to data from the Consumer Financial Protection Bureau (CFPB), the average interest rate differential between dealer-arranged financing and direct lending can be 1.5 to 2.5 percentage points. Over a $20,000 loan, that gap costs borrowers between $800 and $1,800 in additional interest. Refinancing closes that gap.

The break-even calculation matters too. If refinancing costs you $300 in fees and saves you $60 per month, you break even in five months — after that, every payment is net savings. Use that math before committing.

Where to Find the Best Refinancing Rates

The lender landscape for auto refinancing is broader than most people realize. Here are the main categories worth exploring:

- Credit unions consistently offer the most competitive auto loan rates, often 1–2% below banks. Membership requirements have loosened considerably — many credit unions allow anyone in a geographic region or professional field to join with a small deposit.

- Online lenders like LightStream, PenFed Credit Union (which operates nationally online), and RefiJet specialize in auto refinancing. They offer fast decisions and competitive rates, particularly for borrowers with good to excellent credit.

- Your existing bank or credit union may offer loyalty discounts on refinancing, especially if you have a checking or savings account in good standing.

- Marketplace platforms such as LendingTree or AutoPay let you submit one application and receive multiple competing offers simultaneously. This is highly efficient, and multiple inquiries within a 14-day window typically count as a single hard pull on your credit report under FICO scoring models.

Rate shopping for two weeks won’t tank your credit — but skipping it entirely might cost you $500 or more in unnecessary interest. It’s worth the hour it takes to compare three or four offers side by side.

When reviewing offers, pay close attention to whether any lender charges an origination fee or builds costs into the APR differently. Two lenders quoting the same nominal rate can deliver different actual costs depending on how fees are structured. Always compare the total amount repaid over the full remaining term — not just the monthly figure — to get a true apples-to-apples comparison.

Step-by-Step: How to Refinance Your Auto Loan

The process involves fewer steps than a mortgage refinance and typically closes within a week. Here’s what to expect:

- Pull your credit report and score. Free access is available through AnnualCreditReport.com. Know where you stand before lenders run their own checks.

- Gather your loan details. You’ll need your current lender’s name, the payoff amount (not just the balance), remaining term, and current interest rate.

- Get your vehicle information. Lenders will need the VIN, mileage, make, model, and year. Most have maximum mileage and vehicle age cutoffs — typically under 150,000 miles and no older than 10 years, though this varies.

- Submit applications within a short window. Aim to complete all applications within 14 days to minimize credit score impact.

- Compare the actual APR, not just the monthly payment. A lower payment achieved by extending the term isn’t necessarily a better deal — it may cost you more overall.

- Accept the best offer and complete the paperwork. The new lender sends the payoff amount directly to your old lender, and you begin payments on the new loan. Continue paying your old loan until you confirm the payoff is complete — gaps in payment can create late marks on your credit history.

If managing multiple debts is part of your broader challenge, it may also be worth reading student loan payoff strategies that actually work — many of the prioritization principles translate directly to auto debt management.

Credit Score Impact and What to Watch For

Refinancing has a nuanced effect on your credit. On one hand, the hard inquiry from each lender application temporarily drops your score by a few points. On the other, closing an old account and opening a new one can affect your average account age — a factor that makes up about 15% of a FICO score. If your credit file is thin, this impact is more pronounced.

The upside: making on-time payments on the new loan rebuilds that credit health steadily. For most borrowers with an established credit history, the short-term dip from refinancing is negligible compared to the financial benefit of a lower rate.

One thing to watch: some borrowers refinance while also carrying high credit card balances. That combination signals higher risk to lenders and may result in a less favorable rate. If you’re working to reduce revolving debt at the same time, pay attention to the hidden credit card fees you should avoid — they can quietly inflate your balance and undercut your refinancing profile.

It’s also worth thinking about how auto debt fits into your broader financial picture. The financial goals to set in your twenties, thirties, and forties offers a useful framework for prioritizing debt reduction alongside other life-stage priorities — something I’ve found helpful when advising readers who feel pulled in too many directions at once.

For additional perspective on how lenders evaluate overall creditworthiness, understanding your full cost of living obligations — including insurance — can strengthen your case when approaching lenders for a refinance.

Conclusion

Refinancing an auto loan isn’t a financial trick — it’s a corrective move that fixes a deal you probably made under less-than-ideal conditions. The borrowers who benefit most are those who’ve improved their credit, originally financed through a dealership, or who simply never shopped rates in the first place. Take an afternoon to pull your loan details, check your credit score, and request quotes from two or three lenders. If the rate differential saves you more than any fees charged, sign and move on — you’ve just put real money back in your pocket without changing your behavior by a single dollar.

FAQ

How much does refinancing an auto loan typically save?

Savings vary widely depending on your current rate, credit score, remaining loan balance, and new rate. In practical terms, borrowers who refinance from a dealership-arranged rate to a direct lender rate frequently save between $500 and $2,500 over the remaining loan term. The bigger the rate gap and the more months remaining, the larger the benefit.

Will refinancing hurt my credit score?

Each hard inquiry from a lender application causes a small, temporary score drop — usually 2 to 5 points. If you apply with multiple lenders within 14 days, FICO typically counts these as one inquiry. Over time, consistent on-time payments on the new loan rebuild any minor credit impact.

How soon after getting a car loan can I refinance?

Most lenders require that your current loan is at least 60 to 90 days old before they’ll refinance it. Waiting 6 to 12 months is often smarter — it gives you time to build a payment track record and allows any credit score improvements to materialize before you apply.

Are there fees involved in refinancing an auto loan?

Some lenders charge origination fees, and your state may require a title transfer fee when the lienholder changes — typically $15 to $75. Check whether your existing loan has a prepayment penalty, which some lenders include in the original contract. Add all of these costs to your break-even calculation.

What credit score do I need to refinance my auto loan?

Most lenders consider applicants with scores of 600 or above, but the best rates — typically reserved for borrowers in the “prime” or “super-prime” tiers — require scores of 720 or higher. That said, even moving from 620 to 660 can shift you into a meaningfully better rate bracket at many credit unions and online lenders.

Can I refinance if my car has high mileage?

High mileage is one of the most common reasons lenders decline auto refinance applications. Most set a hard ceiling somewhere between 100,000 and 150,000 miles, though cutoffs vary by institution. If your vehicle is approaching those thresholds, apply sooner rather than later — and prioritize lenders who specialize in used vehicle financing, as they tend to have more flexible policies than traditional banks.

Daniel Cross is a financial writer and structural analyst focused on long-term market forces, systemic risk, and the incentives that shape real financial outcomes. His work emphasizes clarity, realism, and context over short-term market noise or speculative narratives.