Most people check their credit card statement once a month, scan for the total, and move on. That habit costs the average American cardholder more than they realize — the Consumer Financial Protection Bureau reported that U.S. consumers paid over $14 billion in credit card fees and penalty charges in a single recent year, and a significant share of that came from charges cardholders didn’t fully understand when they signed up. Hidden credit card fees are rarely buried in fine print by accident; they’re structured to be easy to miss and even easier to trigger.

This guide breaks down the fees that catch people off guard most often, explains how each one works mechanically, and gives you concrete ways to sidestep them. No guarantees of saving a specific dollar amount — fee exposure varies by card and spending habits — but understanding these charges is the first step to keeping more of your money where it belongs.

The Annual Fee Trap: Paying for Benefits You Don’t Use

Annual fees get the most press, yet they remain one of the most commonly mismanaged charges. Cards with annual fees range from $25 on entry-level products to $695 on premium travel cards. The problem isn’t the fee itself — it’s cardholders who pay it year after year while barely using the benefits tied to it.

I’ve spoken with people who held a $550-a-year card for the airport lounge access, then realized they flew domestically maybe twice a year and the lounge was in a terminal they never used. The math didn’t work. A good rule: calculate the dollar value of benefits you actually use, not the marketed value. If you’re genuinely redeeming lounge access, travel credits, and dining perks that add up to more than the annual fee, keep the card. If the card is mostly sitting in your wallet, the fee is pure loss.

Some issuers will waive or downgrade your card to a no-fee version if you call and ask. It’s worth the 10-minute phone call — especially if you’ve been a customer for multiple years. If you’re comparing cashback options, the best cashback credit cards for everyday spending can help you find products where fee structures actually align with how you spend.

Another angle worth considering: some premium cards offer statement credits that effectively offset a large portion of the annual fee — but only if you remember to use them. Credits for streaming services, rideshare, or hotel bookings often expire on a calendar year basis, not your card anniversary. Build a reminder into your routine to capture every credit you’ve earned. Leaving a $50 dining credit unused because you forgot it existed is the same as paying $50 extra for the card.

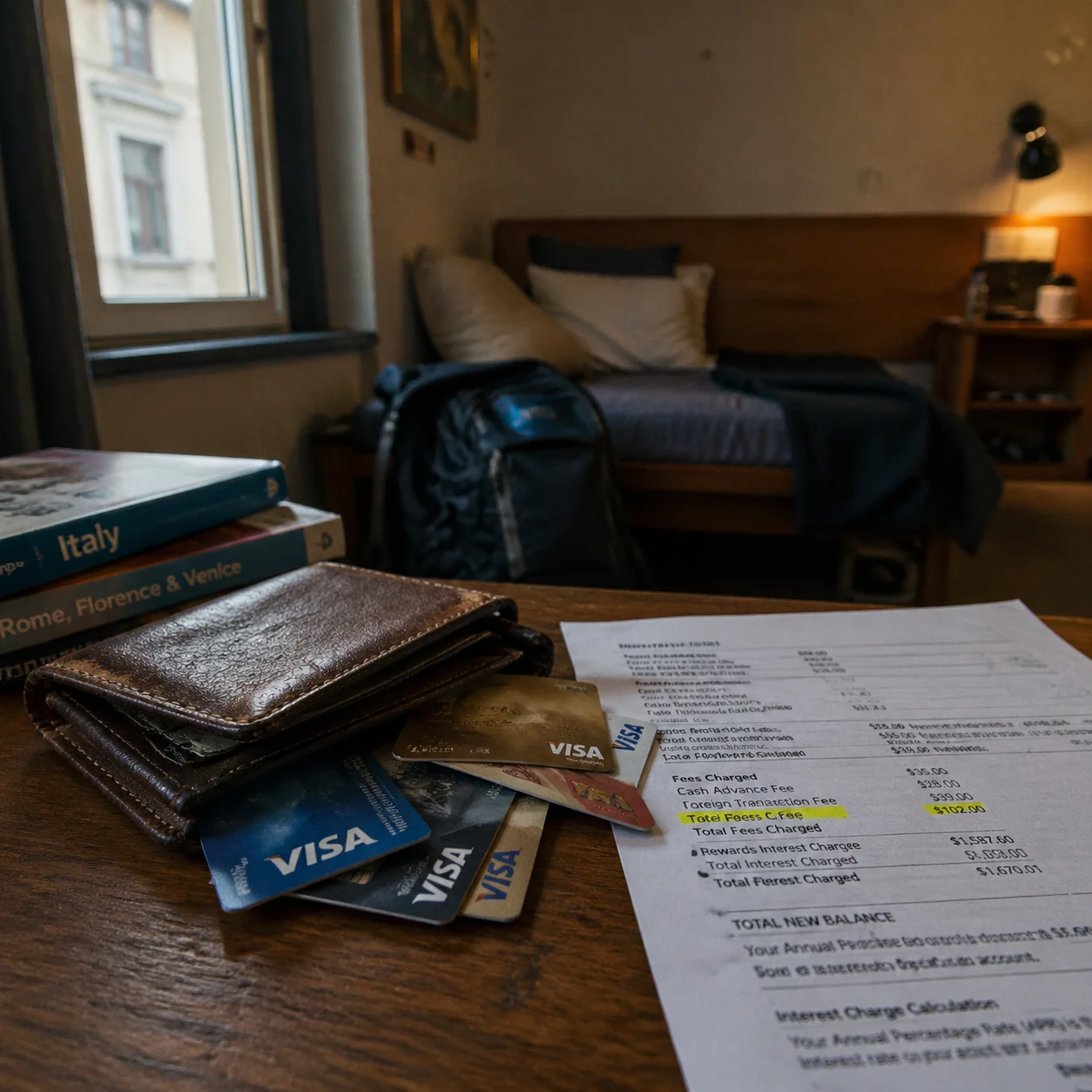

Foreign Transaction Fees: The Tax on Traveling

Foreign transaction fees typically run between 1% and 3% of each purchase made in a foreign currency or processed through a foreign bank. Three percent sounds trivial until you’re spending $4,000 on a two-week trip abroad — that’s $120 quietly added to your bill for the privilege of using your card overseas.

What catches many people off guard is that these fees can apply even when you’re shopping online from a U.S. address, if the merchant processes payments through a foreign bank. Buying something from a European retailer’s website while sitting at home in Ohio can still trigger the fee.

The straightforward fix is to carry a card with no foreign transaction fee when traveling or shopping internationally. Dozens of cards — including many no-annual-fee options — have eliminated this charge entirely. Check your current card’s terms before booking any international trip. If your primary card charges 3%, opening a travel-focused card before the trip is worth considering. For a curated look at cards built for this exact scenario, the best travel rewards credit cards for 2026 covers options with strong international protections.

One often-overlooked related pitfall is dynamic currency conversion (DCC). When you’re abroad and a merchant’s payment terminal asks whether you’d like to pay in your home currency rather than the local one, choosing your home currency sounds convenient but almost always results in a worse exchange rate set by the merchant — sometimes worse than the foreign transaction fee you were trying to avoid. Always choose to pay in the local currency and let your card handle the conversion.

Cash Advance Fees and the Double Penalty Nobody Talks About

Using your credit card at an ATM or to cover a wire transfer triggers a cash advance — and the fee structure is deliberately punishing. Most issuers charge either a flat fee (often $10 to $15) or a percentage of the amount (typically 3% to 5%), whichever is higher. On a $500 cash advance, that’s already $25 out of pocket before you’ve spent a dollar.

The second penalty is interest. Unlike regular purchases, cash advances have no grace period. Interest starts accruing the moment the transaction posts, often at a separate APR that’s higher than your purchase rate — commonly 25% to 30%. If you carry that $500 balance for two months, you’re looking at meaningful interest charges stacked on top of the upfront fee.

Beyond ATM withdrawals, cash advance treatment often applies to things that don’t obviously feel like cash advances: buying lottery tickets, loading prepaid cards, purchasing cryptocurrency through certain platforms, and sending money via payment apps that process through your credit card as a cash advance rather than a purchase. Read the transaction type before confirming anything that involves transferring value rather than buying a product or service.

Balance Transfer Fees: When Moving Debt Costs You

Balance transfers are frequently marketed as a smart debt management strategy, and they can be — but the fee attached often gets glossed over in the headline “0% APR for 15 months” offer. Most balance transfer fees sit at 3% to 5% of the transferred amount. On a $6,000 balance, that’s $180 to $300 charged immediately.

That fee isn’t inherently bad if the math still favors the move. If you’re currently paying 22% APR on a $6,000 balance and you can transfer to a 0% card for 18 months with a 3% fee, the $180 fee is almost certainly worth it compared to the interest you’d otherwise pay. The problem arises when people don’t do that math — they see “0% interest” and assume the transfer is free, then get surprised by the charge on their first statement.

A few cards offer 0% balance transfer fees as a promotional feature. They’re less common, but they exist. When comparing options, factor the transfer fee into your total cost calculation, not just the promotional APR period. Also confirm whether the promotional rate applies to new purchases or only to transferred balances — those are often treated separately.

Timing matters, too. Most issuers require you to complete the balance transfer within a defined window after account opening — typically 60 to 120 days — to qualify for the promotional rate. Missing that window means your transferred balance accrues interest at the standard purchase or cash advance APR, which erases most or all of the benefit you were pursuing in the first place.

Late Payment Fees and the Rate Penalty That Follows

A missed payment triggers two distinct consequences that most people treat as one event. The first is the late fee itself: federal law caps it at $8 for a first offense under recent CFPB rulemaking (though issuers have challenged this in court and the regulatory landscape is still evolving — check current rules for your specific card). Before those caps, issuers were charging up to $41.

The second consequence is more damaging: the penalty APR. Most credit card agreements include a clause allowing the issuer to raise your interest rate to a penalty rate — often 29.99% — if you miss a payment or make a late payment. That penalty rate can apply to your existing balance, not just future charges, depending on your cardmember agreement. And it can stay in place for a minimum of six consecutive on-time payments before the issuer is required to review it.

Autopay for at least the minimum payment amount eliminates this risk. If cash flow is genuinely tight and autopay isn’t manageable, set a calendar alert three days before your due date. Some issuers also offer due date flexibility — you can shift your billing cycle to align with your paycheck schedule. Call and ask; it’s a legitimate option that many cardholders don’t know exists.

If fee-related debt has already compounded into a broader credit problem, understanding your options through how to get a loan with bad credit can help you assess refinancing paths.

Over-the-Limit Fees and Minimum Interest Charges

Over-the-limit fees were once automatic, but the Credit CARD Act of 2009 required issuers to get your explicit opt-in before charging them. If you never opted in, your card will typically decline rather than approve a charge that exceeds your credit limit. Still, some cardholders opted in years ago during sign-up without registering it — and some cards market this as a “benefit” called flexible spending. Check whether you’ve opted in, because if you have, exceeding your limit triggers a fee that typically runs between $25 and $40.

Minimum interest charges are a separate, lesser-known irritant. Some cards specify a minimum interest charge — often $1 to $2 — that applies whenever you carry any balance at all, even a tiny one. If you accidentally let $8 roll over to the next month, you might pay $1.50 in interest when the math would suggest it should be pennies. It’s a small amount, but it signals that carrying any balance at all, however small, comes with a floor cost.

Both of these charges are disclosed in your Schumer Box — the standardized fee table that every card issuer must provide. Reading that table before you apply, not after, gives you a complete picture of what you’re agreeing to. A broader approach to reducing monthly expenses without sacrificing quality pairs well with tightening up credit card cost management.

Conclusion

Credit card fees are not random — each one exists because issuers have found that a meaningful percentage of cardholders will trigger it, pay it, and not change their behavior. The most effective defense is reading your Schumer Box before you apply, setting autopay to avoid late penalties, and auditing your annual fee cards once a year to confirm you’re still getting value. Pick one card statement you’ve never read closely and go through every line item this week. What you find there may reframe how you manage every card you carry.

FAQ

What is the most common hidden credit card fee?

Foreign transaction fees and cash advance fees are among the most frequently overlooked charges. Many cardholders don’t realize foreign transaction fees can apply to online purchases from foreign merchants, even when made from home.

Can I negotiate credit card fees with my issuer?

Yes, in many cases. Calling your issuer and politely requesting a fee waiver — especially for a one-time late fee if you have a strong payment history — works more often than most people expect. Annual fee waivers or product downgrades are also commonly available upon request.

Does a cash advance hurt my credit score?

The cash advance itself doesn’t appear as a separate negative mark, but it increases your credit utilization ratio, which can lower your score. The high APR that immediately accrues also increases the risk of carrying a growing balance, which compounds the utilization impact over time.

How do I find all the fees on my credit card?

Look for the Schumer Box — a standardized table required by federal law on all credit card applications and agreements. It lists APRs, fees, and penalty rates in a uniform format. Your current card’s Schumer Box is available in your online account under “Terms and Conditions” or “Pricing and Terms.”

Is it worth getting a card just to avoid foreign transaction fees?

If you travel internationally more than once a year or regularly shop from foreign merchants online, yes. Many no-annual-fee cards now include no foreign transaction fees, so there’s no cost to holding one as a secondary card specifically for international use.

What is dynamic currency conversion and should I avoid it?

Dynamic currency conversion (DCC) is when a foreign merchant offers to charge you in your home currency instead of the local one. It sounds convenient, but the exchange rate applied is set by the merchant and is almost always less favorable than what your card network would apply. Declining DCC and paying in local currency is nearly always the better financial choice, even if your card charges a foreign transaction fee.

Daniel Cross is a financial writer and structural analyst focused on long-term market forces, systemic risk, and the incentives that shape real financial outcomes. His work emphasizes clarity, realism, and context over short-term market noise or speculative narratives.